Monthly Income of at least 150,000 kyats (Minimum annual income MMK 1,800,000/- or

MOB provides Sight LC and Usance LC to trade customers. MOB bank facilitates the

Higher rate of interest than savings account until maturity date. Interest can be transferred to

Using our trustee services , MOB, as a trustee , holds funds of the customers

MOB received Merchant Service & Trademark License Agreement from UnionPay International (UPI) on 24th December 2015 and started issuing MOB UnionPay Co-brand Credit Card

In line with a partnership agreement between Western Union (WU) and MOB, MOB has provided WU Money Transfer Service to its customers since 2012.

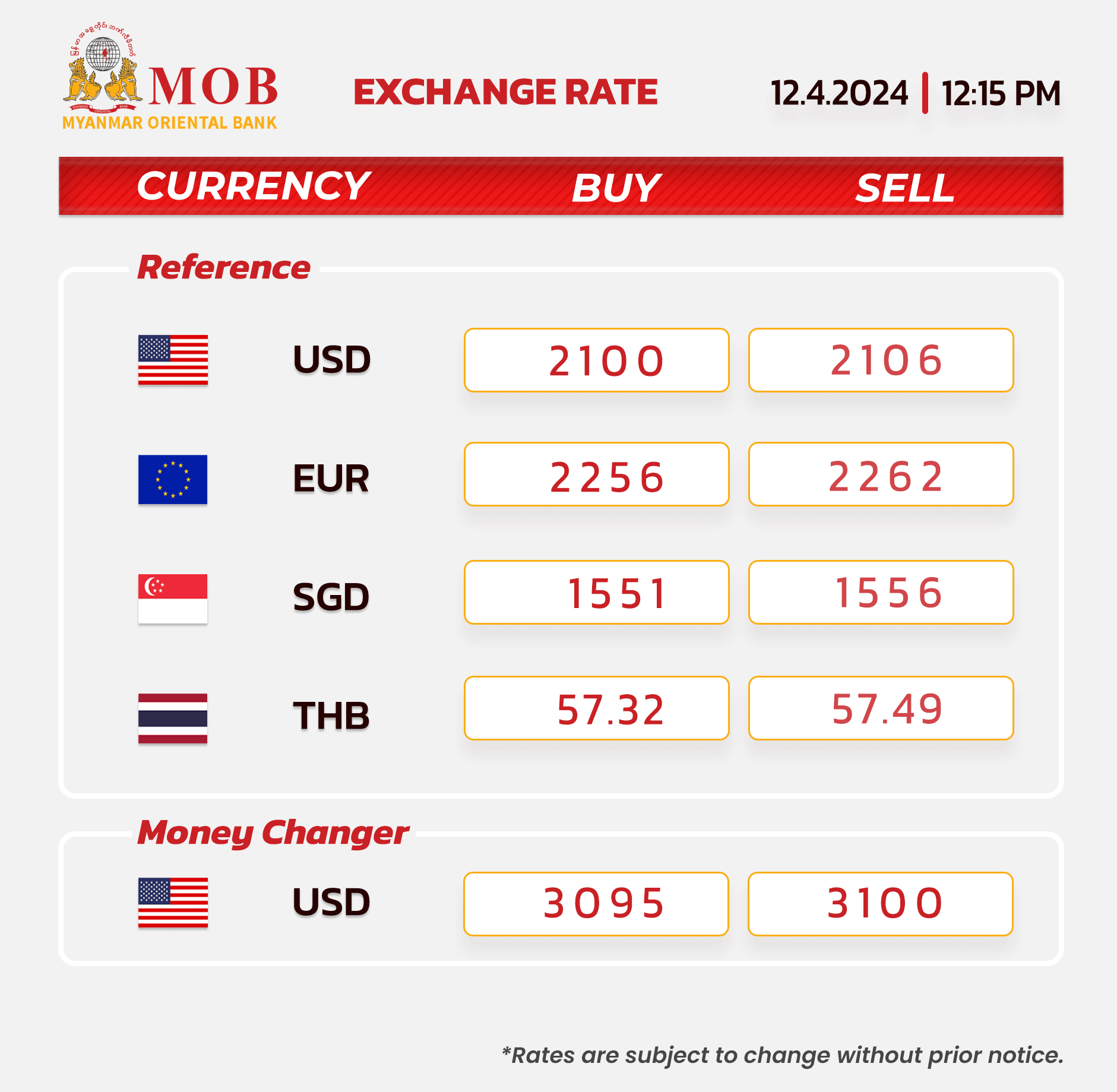

ပြည်ပသို့ ထွက်ခွာသူများအား အသေးသုံးနိုင်ငံခြားငွေ ငွေသားရောင်းချပေးခြင်း။

မြန်မာအရှေ့တိုင်းဘဏ် (MOB) နှင့် ဆက်သွယ်ဆောင်ရွက်လျက်ရှိသော မိတ်ဟောင်း၊မိတ်သစ် Customers လူကြီးမင်းများအား သတင်းကောင်းပါးပါရစေရှင်...

MOB 29TH ANNIVERSARY FIXED DEPOSIT PROMOTION

မြန်မာအရှေ့တိုင်းဘဏ် (MOB) ၏ (၁၈.၁၁.၂၀၂၂) နေ့တွင် ကျရောက်မည့် (၂၉)နှစ်မြောက် နှစ်ပတ်လည်...

အသိပေးကြေညာခြင်း

Western Union ငွေလွှဲအပါအဝင် ပြည်ပရောက် မြန်မာနိုင်ငံသားများအတွက် မိမိတို့၏မိသားစုများထံသို့ ပြည်ပမှ ငွေလွှဲပို့မှုများအတွက်...